Powered by the real-time trading data in our CIX VCM Trade Database, the quarterly CIX Intelligence Market Pulse condenses thousands of daily price points into signals market participants need to navigate an evolving voluntary carbon landscape.

Our Q1 2025 Market Pulse edition shows a market in transition: buyer preferences are shifting away from traditional forest protection credits towards a more diversified mix of reductions and removals, while prices diverge sharply across benchmarks and geographies.

Disclaimer: This following analysis reflects a subset of market activity and is intended for indicative purposes only.

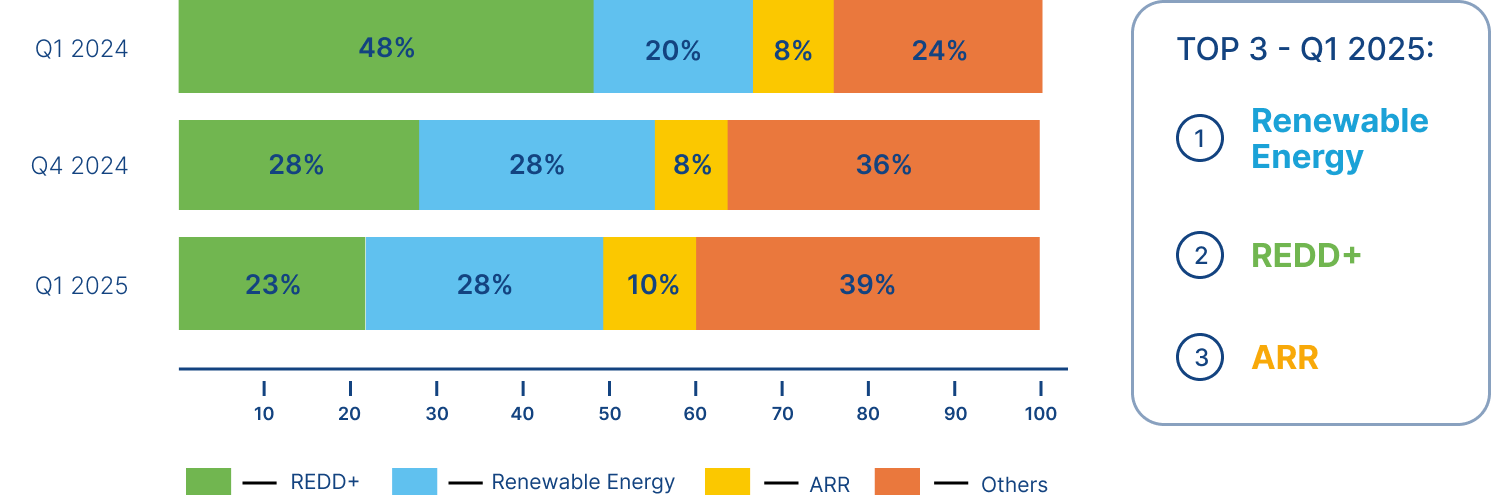

TOP 3 MOST ACTIVE CREDIT TYPES

Renewable Energy, REDD+, and Afforestation, Reforestation and Revegetation (ARR) credits continue to dominate the voluntary carbon market (VCM), accounting for over 60% of trading activity (e.g. transactions, bids, offers)—but momentum is shifting.

REDD+ has seen a sharp decline, with trading activity falling to 23% in Q1 2025, down from 48% a year earlier. This reflects a cooling in demand for forest-based reduction credits amid scrutiny and evolving buyer preferences. In contrast, renewable energy and ARR are gaining ground. While still a smaller segment, ARR’s steady growth suggests a rising appetite for long-term carbon removal solutions.

TOP 3 EMERGING CREDIT TYPES

A new wave of credit types is steadily gaining traction. Improved Forest Management (IFM), landfill methane and waste management projects have shown consistent year-over-year growth in trading activity, suggesting a diversification in project demand and a broadening definition of climate impact. As confidence and scrutiny increase in equal measure, buyers are diversifying portfolios—balancing reductions and removals, nature-based and engineered solutions—in pursuit of credible, scalable climate action.

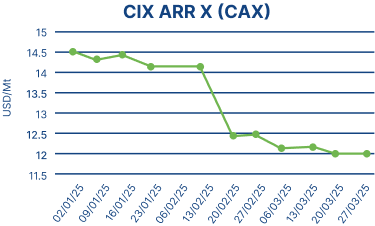

CIX BENCHMARK MOVEMENTS

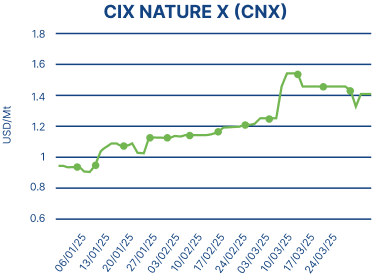

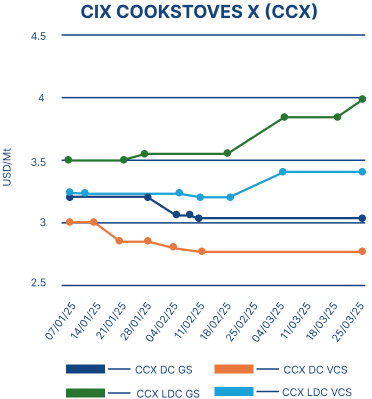

Note: The CAX and CNX benchmark contracts are vintage 2021, while the CCX contract is vintage 2022.

The CIX ARR X (CAX) benchmark held steady at around US$14.25 through the first half of Q1 2025, before dipping and eventually settling at US$12.00.

The CIX Nature X (CNX) benchmark for REDD+ projects saw an increase at the beginning of the year before stabilising at around US$1.40—showing modest but positive movement, albeit amid limited spot liquidity for the prevailing 2021 vintage.

The four CIX Cookstoves X (CCX) benchmarks saw a notable divergence. Prices in Least Developed Countries (LDCs) broke away from those in Developing Countries (DCs) mid-quarter and continued to climb through to the end of March.

One possible interpretation is that developers operating in LDCs may be withholding supply in anticipation of accessing the higher-priced CORSIA market, as these countries are more likely to issue the Letters of Authorisation (LOAs) needed for eligibility.

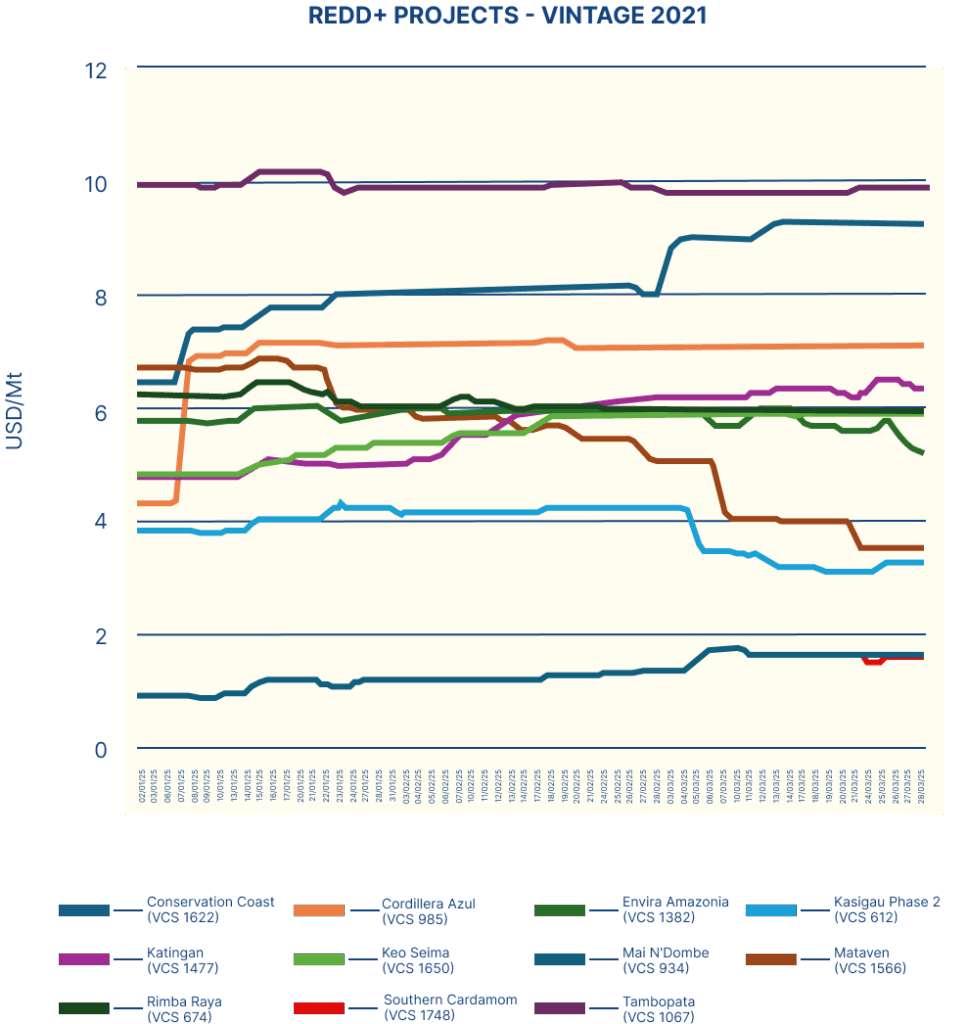

REDD+ MARKET MOVEMENTS

Even though the CNX benchmark posted gains over Q1 2025, price movements across individual REDD+ projects have been mixed. Katingan and Keo Seima (v21) credits recorded quarter-over-quarter increases, while Mataven values declined and Rimba Raya saw a more recent decline. This highlights the variability in pricing performance even within a single credit category.

Want to dive deeper?

CIX Intelligence is a market data and analytics service for environmental markets. Designed to inform market-wide decision making and elevate price transparency, it features thousands of historical and daily updated price points, including project specific bids, offers and trades from the spot market and proprietary data from CIX venues.

The service also includes CIX’s growing suite of on-screen driven price benchmarks spanning the most active carbon market segments.

For queries on specific project-level prices or benchmarks, reach out to us below.

Let’s Connect

Ready to discover the right price of carbon credits? Let’s connect.

Market Intelligence

"*" indicates required fields