Powered by the real-time trading data in our CIX VCM Trade Database, the quarterly CIX Intelligence Market Pulse condenses thousands of daily price points into signals market participants need to navigate an evolving voluntary carbon landscape.

Disclaimer: This following analysis reflects a subset of market activity and is intended for indicative purposes only.

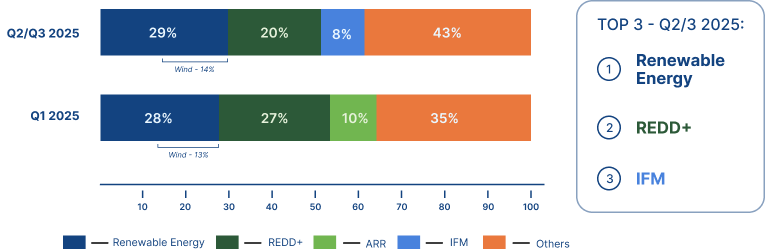

TOP 3 MOST ACTIVE CREDIT TYPES

While renewable energy and REDD+ remain the top two most active credit types in the VCM, IFM overtook ARR in Q2 and Q3 as the third most active credit type, reaching 8.32% of market activity. Recorded ARR activity fell from 9.44% in Q1 to 7.87% in Q2-3. REDD+ share of market activity continues to decrease, falling to 20% in Q2 and Q3 from 27% in Q1. Wind energy continues to be the most active technology type within renewable energy.

MARKET TRENDS BY CREDIT TYPE

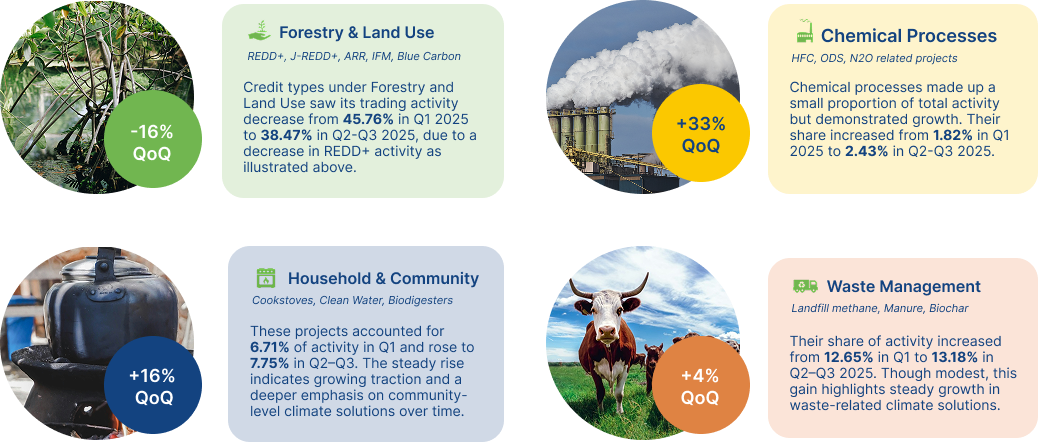

In Q2 and Q3 2025, the Forestry and Land Use segment saw a 16% decrease in recorded market activity, driven primarily by the decrease in project-based REDD+ activity. Meanwhile, activity in the Chemical Processes, Household and Community, and Waste Management segments increased by 33%, 16%, and 4%, respectively.

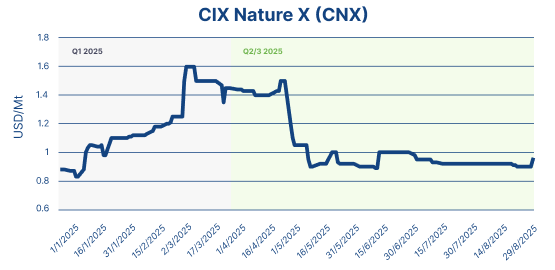

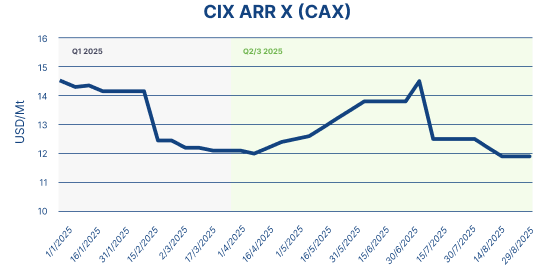

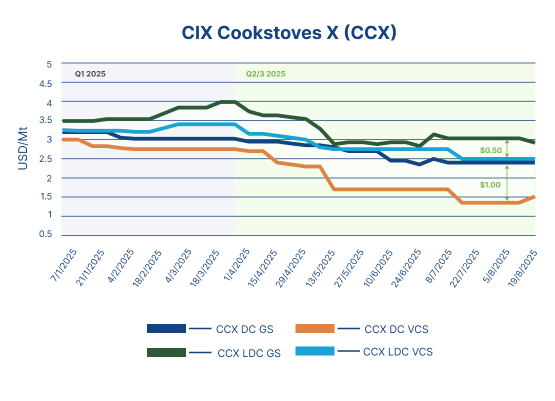

CIX BENCHMARK MOVEMENTS

Note: The CAX and CNX benchmark contracts are vintage 2021, while the CCX contract is vintage 2022.

The CIX Nature X (CNX) benchmark fell midway through Q2 before stabilising at around $0.90, where it has remained through Q3 so far, reflecting muted activity throughout the summer for Southern Cardamom (VCS 1748).

The CIX ARR X (CAX) benchmark increased throughout Q2 and reached a peak of $14.25 at the end of Q2 before falling to $12.00 again in Q3, driven by changing supply dynamics and a new quality rating for the basket’s current clearing project.

For cookstoves, the CIX Cookstoves X (CCX) Least Developed Countries Gold Standard (CCX LDC GS) benchmark and Developing Countries Verra (CCX DC VCS) benchmark fell sharply in Q2, while the LDC VCS and DC GS contracts decreased more gradually.

A wide spread has emerged between the Gold Standard and Verra assessments of both the LDC and DC contracts, with the gap for LDC contracts at about $0.50 and for DC contracts at about $1.00.

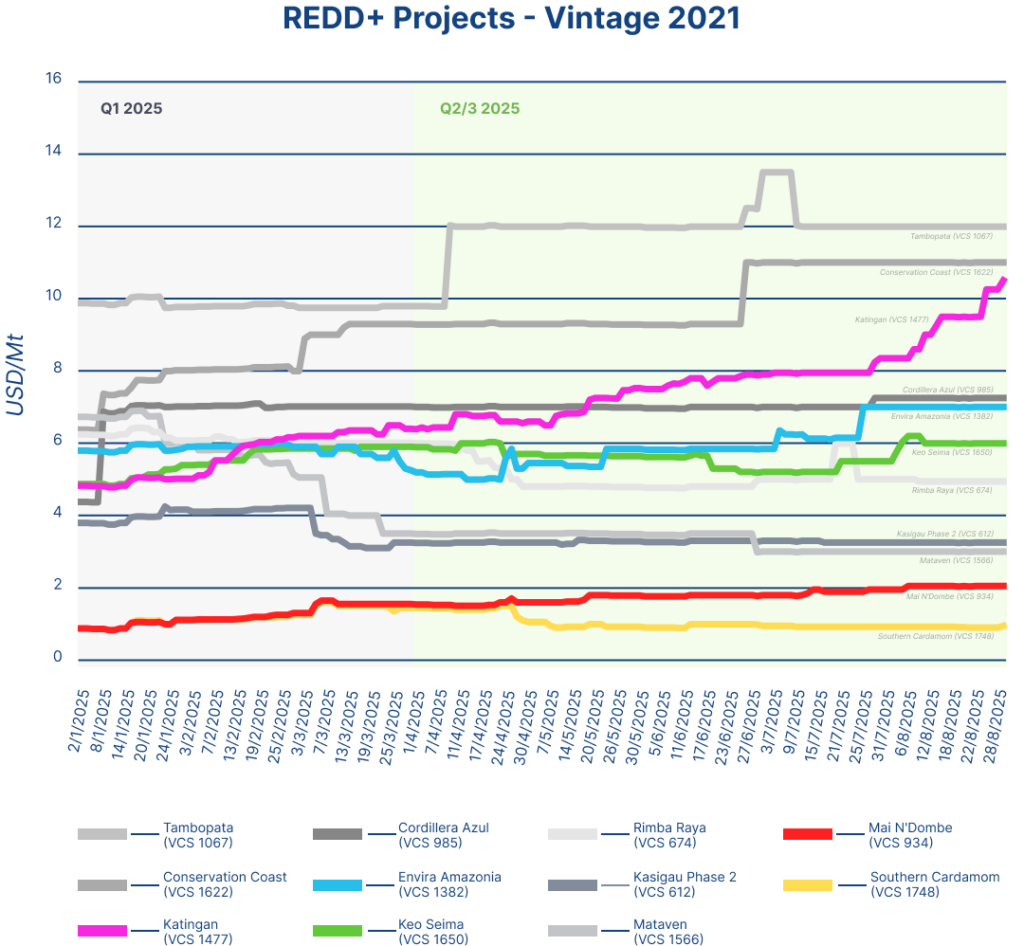

REDD+ MARKET MOVEMENTS

While the CIX Nature X benchmark fell over the monitoring period, a few basket projects saw mixed movements, reinforcing the trend that activity in the REDD+ market is driven by a select handful of projects.

Katingan (VCS 1477) saw a steady increase in value through Q2 and Q3, surging to over $10 in value in late August, up from $6 at the start of Q2. Envira (VCS 1382) and Keo Seima (VCS 1650) saw mixed movements, with Envira reaching about $7.00 and Keo Seima staying more stable at $6.00. Southern Cardamom and Mai N’Dombe (VCS 934) diverged in value through Q2 and Q3, with Mai N’Dombe climbing to nearly $2.00 while Southern Cardamom has stayed depressed at below $1.00.

Want to dive deeper?

CIX Intelligence is a market data and analytics service for environmental markets. Designed to inform market-wide decision making and elevate price transparency, it features thousands of historical and daily updated price points, including project specific bids, offers and trades from the spot market and proprietary data from CIX venues.

The service also includes CIX’s growing suite of on-screen driven price benchmarks spanning the most active carbon market segments.

For queries on specific project-level prices or benchmarks, reach out to us below.

Let’s Connect

Ready to discover the right price of carbon credits? Let’s connect.

Market Intelligence

"*" indicates required fields