Carbon taxation is becoming an increasingly common policy tool worldwide. Singapore’s approach offers insights into how companies everywhere can prepare for rising carbon costs while unlocking new opportunities.

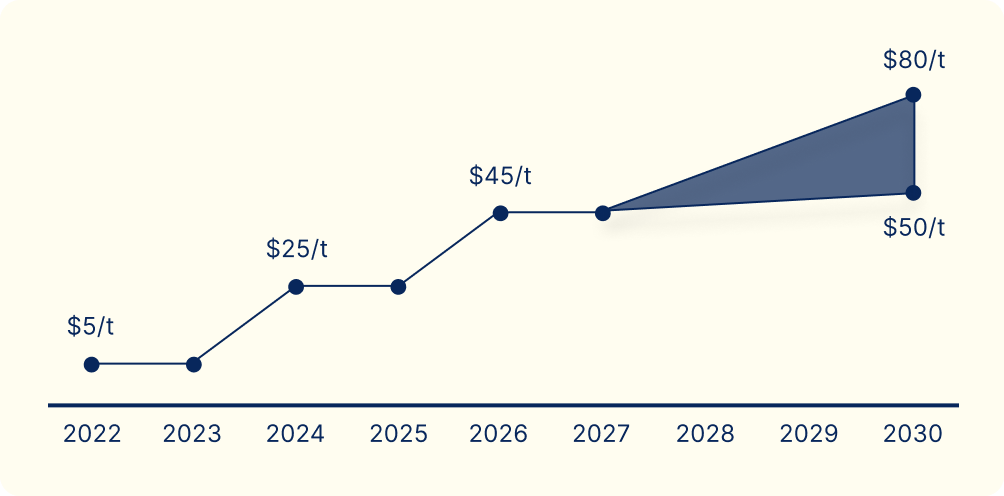

When Singapore raised its carbon tax in 2024 from S$5 to S$25 per tonne of emissions, many companies anticipated cost pressures. The trajectory is clear: rates will increase to S$45 for 2026-27, with a view toward S$50-80 by 2030. Facilities emitting 25,000 tonnes or more of CO₂-equivalent annually — around 50 plants across power generation, manufacturing, and waste — fall under the regime, accounting for about 70% of the nation’s greenhouse gas emissions1.

While the policy introduces costs, it also creates opportunity. By weaving compliance into business strategy, companies can shift from reactive cost management to proactive value creation. Five areas stand out:

1. Turning costs into predictable line items

Unlike volatile energy or commodity markets, Singapore’s carbon tax follows a transparent trajectory. This allows finance teams to forecast liabilities and treat carbon as a budgetable cost. For example, cutting 10,000 tonnes of emissions annually avoids S$800,000 in exposure once rates reach S$80. Such visibility strengthens the business case for low-carbon investments.

Instead of viewing compliance as a burden, companies have several practical levers to make carbon a controllable and strategic cost:

- Adopt internal carbon pricing (ICP): Over 2,000 companies globally now use or plan to use ICP, enabling them to model future carbon costs and prioritise low-carbon projects that remain financially resilient2.

- Embed carbon in financial planning and capex decisions: By incorporating carbon costs into investment criteria, businesses ensure that climate-friendly projects are evaluated alongside traditional metrics, increasing the likelihood of approval.

- Leverage International Carbon Credits (ICCs): Singapore allows up to 5% of taxable emissions to be offset with ICCs, often at lower cost than the tax itself3. Securing high-quality credits early reduces compliance costs and mitigates supply risks.

By integrating these approaches, companies shift carbon management from a residual risk into a deliberate financial strategy. Partners like Climate Impact X (CIX) provide corporates with access to environmental markets, flexible transaction modalities, and market intelligence, enabling carbon to be managed as part of financial strategy rather than a residual risk.

2. Operational efficiency: decarbonisation as cost reduction

Preparing for compliance requires robust monitoring, reporting, and verification (MRV). While sometimes seen as administrative, these processes bring data discipline that often reveals operational inefficiencies.

Many emissions-reduction measures double as cost-reduction measures. Energy-efficient upgrades, waste-heat recovery, and process optimisation can cut emissions with paybacks of one to two years, even before higher tax rates take effect. McKinsey notes that many firms are finding projects that improve EBITDA while lowering emissions4.

Compliance also strengthens governance, embedding audits, data checks, and controls that reduce both reputational and financial risk. In short, preparing for the carbon tax both sharpens oversight and unlocks efficiency savings well before carbon reaches S$80 by 2030.

3. Strategic alignment with net-zero goals

Singapore’s tax underpins its national net-zero 2050 commitment. For businesses, this means today’s carbon costs preview a future where emissions are increasingly penalised. Companies that delay may find themselves facing steep tax bills with few quick abatement options, especially once Singapore’s temporary ‘transition allowances’ — partial rebates that soften the tax for emissions-intensive industries — are phased out.

Integrating compliance with corporate climate strategies ensures that each dollar spent on emissions-reduction measures also advances long-term net-zero pathways. Renewable energy investments, electrification, or process redesign can thus be justified as both tax avoidance and strategic alignment.

Acting early reduces the risk of stranded assets. Firms that spread investments over time can transition smoothly, avoiding the financial and operational disruption of rushed last-minute changes.

4. Investor and stakeholder confidence

In the eyes of investors, banks, and business partners, carbon management is increasingly a marker of good leadership and resilience. A company with a credible plan to cut taxable emissions by 50% by 2030 signals operational resilience, carbon cost foresight, and fewer regulatory surprises. Credibility can be built on three main fronts:

- Investor expectations: Companies that demonstrate proactive management gain credibility and may enjoy lower financing costs or better access to sustainability-linked capital. BlackRock and other asset managers explicitly ask firms to set and deliver on credible net-zero plans5.

- Supply chain and customer pressures: Multinationals with Science Based Targets are requiring suppliers to disclose and cut emissions, raising the bar for participation in global value chains.

- Disclosure standards: Frameworks like TCFD and ISSB now expect companies to model scenarios with explicit carbon prices, making internal carbon pricing and scenario analysis critical to credibility6.

In short, robust carbon management turns compliance into a competitive signal of resilience and foresight.

5. Unlocking market opportunities

Finally, embracing the carbon tax early can act as a gateway to new market opportunities. In Singapore’s case, the government’s decision to allow limited use of international credits has implicitly invited companies to engage with carbon markets. By engaging in the market to source ICCs, companies gain knowledge, relationships, and tools they can later use for voluntary strategies or portfolio hedging. Bain & Company and the World Economic Forum noted in a report that carbon markets can provide the resources for an “orderly transition” and explicitly call on corporations to integrate carbon markets into their climate strategies to drive sustainable growth7.

Early movers can negotiate better terms, secure long-dated supply at favourable prices, and build diversified carbon portfolios. They also acquire know-how in evaluating credit quality, working with counterparties, and managing exposure.

Navigating compliance with Climate Impact X (CIX)

Singapore’s carbon price is set to climb. For corporates, waiting means higher costs and fewer options; acting early transforms tax into strategy. By treating carbon as a predictable line item, driving efficiency, aligning with net zero, strengthening stakeholder trust, and entering new markets, businesses can move from defensive compliance to competitive advantage.

CIX partners with corporates in Singapore to navigate the evolving carbon tax landscape, offering end-to-end solutions to support the integration of International Carbon Credits (ICCs) into compliance strategies. By combining our strategic insights and deep market expertise with our networks and operational capabilities, we translate your compliance requirements into a tangible procurement strategy.

- National Climate Change Secretariat, Singapore’s Carbon Tax overview. https://www.nccs.gov.sg/singapores-climate-action/mitigation-efforts/carbontax/#:~:text=solutions.%20About%2080,1

- CDP (2021), Internal Carbon Pricing Report – Over 2,000 companies use internal carbon prices. https://www.cdp.net/en/insights/nearly-half-of-worlds-biggest-companies-factoring-cost-of-carbon-into-business-plans

- National Climate Change Secretariat, Use of International Carbon Credits (ICCs) under carbon tax. https://www.nccs.gov.sg/singapores-climate-action/mitigation-efforts/carbontax/#:~:text=Use%20of%20International%20Carbon%20Credits

- McKinsey & Co. (2025), Operations’ dual mission as costs of emissions rise – Decarbonization levers with 1–2 year paybacks. https://www.mckinsey.com/capabilities/operations/our-insights/operations-dual-mission-as-costs-of-emissions-rise#:~:text=of%20European%20automotive%20going%2C%20and,pay%20into%20decarbonization%20and%20dematerialization

- McKinsey & Co. (2021), Net Zero or Bust – Pressure on suppliers to cut emissions (SBTi). https://www.mckinsey.com/capabilities/operations/our-insights/net-zero-or-bust-beating-the-abatement-cost-curve-for-growth#:~:text=investments%20accounted%20for%2011%20percent,zero%20emissions%20by%202050

- TCFD Knowledge Hub, Internal Carbon Pricing in Scenario Analysis – TCFD recommendations. https://www.tcfdhub.org/resource/carbon-pricing-and-the-task-force-on-climate-related-financial-disclosures-tcfd/#:~:text=The%20TCFD%20outlines%20recommendations%20to,investment%20decisions%20across%20their%20portfolios

- Bain & World Economic Forum (2025), Asia’s Carbon Markets Report – Corporations urged to use carbon markets in climate strategy. https://www.bain.com/about/media-center/press-releases/20252/integrating-asias-carbon-markets-critical-to-global-net-zero-goals-wef-bain-reports/#:~:text=%E2%80%9CThe%20climate%20finance%20gap%20of,at%20the%20World%20Economic%20Forum