As of May 2026.

About this Guide

This guide was prepared by CIX to help European corporate sustainability, procurement and finance teams navigate Scope 2 EAC purchasing under the EU Corporate Sustainability Reporting Directive (CSRD). It draws on CIX’s operational experience across European and Asia-Pacific (APAC) markets.

Coverage spans Scope 2 EAC procurement for corporate entities operating in the EU-27, the European Economic Area (EEA) and the United Kingdom, with cross-references to APAC certificate markets where relevant for multinationals consolidating Scope 2 disclosures under a single reporting framework.

Table of contents

Executive Summary

- Why Scope 2 Reporting Is Becoming Harder in Europe

- Foundations: Understanding Scope 2 and Guarantees of Origins (GOs)

- CSRD and ESRS E1: Disclosure Requirements and Audit Readiness

- Understanding the European GO Market

- GO procurement strategy

- Future Trends: 24/7 Matching and Granular GO Procurement

- Managing What Guarantees of Origins Cannot Cover

- Industry Deep Dives: Semiconductors and Data Centres

Executive Summary

Scope 2 emissions – those arising from purchased electricity – have long been the most manageable part of a corporate carbon footprint. In Europe, Guarantees of Origin (GOs) provided a recognised, cost-effective mechanism to support renewable electricity claims under the GHG Protocol Scope 2 market-based method. For many organisations, this approach was straightforward: procure certificates, cancel them against consumption and report zero market-based Scope 2. However, this method is no longer sufficient on its own.

The EU Corporate Sustainability Reporting Directive (CSRD) mandates statutory disclosure of both location-based and market-based Scope 2 figures under ESRS E1, with external assurance. The GO instrument is still recognised to support those claims, but must now meet an evidentiary standard comparable to financial data. Procurement decisions that were once internal sustainability choices have become audit-facing commitments.

In parallel, the voluntary frameworks that institutional investors and corporate customers rely on – Carbon Disclosure Project (CDP), the Science Based Targets initiative (SBTi), and RE100 – have raised their electricity procurement quality criteria. Geographic matching, asset vintage and additionality are no longer differentiators but a baseline expectation for credible disclosure.

For data centres and semiconductor manufacturers, the stakes are heightened. Both sectors operate at very high electricity intensity, often at near-continuous load – a profile that makes hourly and 24/7 matching materially harder than annual volumetric matching, even before factoring in acute Scope 3 pressure from downstream customers with their own CSRD obligations.

This guide gives procurement, sustainability and finance teams the technical and regulatory grounding to respond. It covers the GO framework and its integrity criteria, CSRD disclosure obligations in full, procurement structures across fragmented European markets, and the trajectory toward granular 24/7 matching. It also addresses, directly and with evidence, the scepticism around EACs as a legitimate Scope 2 instrument, distinguishing between the weaknesses of low-integrity procurement and the unfounded dismissal of the GO framework as a whole.

For multinationals with material APAC operations, the guide also addresses how I-REC procurement in those markets integrates with European GO data into a single CSRD-compliant Scope 2 disclosure.

1. Why Scope 2 Reporting Is Becoming Harder in Europe

Readers who are new to Scope 2 accounting and renewable energy certificates may find it useful to read Section 2 first, before returning here.

For most of the past decade, corporate renewable electricity procurement in Europe operated within a permissive environment. Published in 2015, the GHG Protocol Scope 2 Guidance introduced the market-based method as a recognised approach to Scope 2 accounting, enabling companies to report lower (and in some cases zero) market-based Scope 2 emissions by retiring Guarantees of Origin (GOs) against their electricity consumption¹. Reporting was voluntary, methodological scrutiny was limited, and unbundled GOs from legacy renewable assets cost a fraction of €1.00 per megawatt-hour. That has changed. Three forces have converged to close that window.

1.1 The tightening regulatory landscape

The Corporate Sustainability Reporting Directive (CSRD), which entered into force in January 2023, is the most consequential change to European corporate sustainability disclosure in a decade². It replaces the Non-Financial Reporting Directive (NFRD), which applied to fewer than 12,000 companies and carried limited methodological prescription, with mandatory, audited sustainability reporting obligations. Under the original CSRD, approximately 40,000-50,000 European entities were projected to fall within scope – a figure since reduced by approximately 80% following the Omnibus I Directive, addressed later³. For Scope 2 specifically, the European Sustainability Reporting Standards (ESRS) introduced under CSRD prescribe two disclosure requirements that directly govern how renewable energy certificates function as a reporting instrument.

ESRS E1-5

Under this disclosure, companies must report their total energy consumption broken down into renewable and non-renewable sources and must use GO cancellation records as evidence for any renewable electricity claims.

ESRS E1-6

Companies must disclose their Scope 2 emissions under the location-based and market-based methods, Both figures are mandatory, and a company cannot present only the market-based figure, however favourable, without disclosing the location-based figure that reflects the physical grid reality. The gap between the two figures is itself a disclosure that investors and auditors will scrutinise.

These disclosures are subject to external assurance. The CSRD framework establishes two levels of assurance stringency, and understanding the distinction is important for how companies build their evidence chains:

- Limited assurance is the mandatory requirement for all in-scope companies. The assurance provider concludes that nothing in the disclosure appears materially wrong – this is known as a negative conclusion, because it confirms the absence of identified problems rather than positively confirming accuracy. Despite being the lower of the two standards, it still requires documentary evidence for every material claim. GO cancellation statements, registry records, residual mix calculations, and the full evidence chain supporting a market-based Scope 2 figure must be audit-ready, not merely plausible. The European Commission is required to adopt formal limited assurance standards by 1 October 2026.

- Reasonable assurance is the higher standard, equivalent to a financial audit, where the assurance provider positively concludes the disclosure is free from material misstatement. Under the original CSRD, the European Commission was empowered to move companies toward this standard in future. That empowerment has since been removed, confirming that limited assurance will remain the applicable requirement for the foreseeable future.

The Omnibus I Directive – enacted law as of March 2026

In February 2025, the European Commission published two parallel legislative proposals constituting what became known as the Omnibus I package. Following a provisional political agreement in December 2025, the Council of the EU formally adopted the final text on 24 February 2026. The Directive was published in the Official Journal of the European Union on 26 February 2026 as Directive (EU) 2026/470 and entered into force on 18 March 2026⁴. Member states have until 19 March 2027 to transpose its CSRD provisions into national law.

The Directive introduces the following substantive changes:

→ Narrowed mandatory scope. Reporting is now required only for large undertakings with more than 1,000 employees AND more than €450M net annual turnover – both thresholds must be metsimultaneously. This reduces the mandatory reporting population by approximately 80% compared to the original CSRD scope.

→ Sector-specific ESRS removed. Standards planned for specific industries have been removed from the mandatory framework entirely. The core sector-agnostic E1-5 and E1-6 obligations remain intact and unchanged. A revised ESRS delegated act aiming to reduce mandatory datapoints while preserving interoperability with global reporting standards is due by 18 September 2026.

→ Wave 2 companies, originally required to report for FY2025, will now first report for FY2027. Wave 3 (listed SMEs) has been removed from mandatory scope entirely, with a voluntary reporting standard to be developed in its place.

→ Reasonable assurance empowerment removed. The Commission’s ability to escalate assurance requirements beyond limited assurance has been eliminated, providing long-term certainty on compliance costs.

| Wave | Entity type | First reporting year | Assurance requirement |

|---|---|---|---|

| Wave 1 | Large public-interest entities (PIEs) >500 employees (banks, insurers, listed companies) | FY2024 – unchanged | Limited assurance; Commission to adopt formal standards by 1 October 2026 |

| Wave 2 | Large undertakings >1,000 employees AND >€450M net turnover (both thresholds must be met) | FY2027 (postponed from FY2025 under Directive (EU) 2026/470) | Limited assurance; escalation to require reasonable assurance removed |

| Wave 3 | Listed SMEs – removed from mandatory scope | No longer mandatory | N/A |

| Wave 4 | Non-EU companies >€450M EU revenues with qualifying EU subsidiary or branch | FY2028 | Limited assurance |

Companies removed from mandatory scope by Directive (EU) 2026/470 may still report voluntarily using a simplified standard currently being developed by the Commission.

Three further developments complete the regulatory picture for 2025–2026:

→ A parallel development: by 21 May 2025, EU member states were required to transpose the Renewable Energy Directive III (RED III) into national law⁵. RED III directly governs how GO registries operate – covering issuance standards, cross-border transfer protocols and cancellation documentation requirements – and its transposition has begun to produce greater standardisation across national registries, though implementation consistency across member states remains uneven. The practical implications of that unevenness for buyers are addressed in Section 1.3.

→ A methodological update to watch: The GHG Protocol Scope 2 Guidance – the 2015 standard on which ESRS E1-6 is built – is currently undergoing its first revision. The first consultation phase concluded in early 2026; a second phase is expected by end of 2026, with the final standard anticipated in 2027–2028⁶. The draft revision proposes to require greater temporal and geographic granularity in how EAC procurement is matched to consumption, changes that would directly affect how market-based Scope 2 figures are calculated and evidenced. The final standard is not yet in force, but companies designing long-term procurement strategies should be building evidence chains and consumption data infrastructure that can accommodate hourly matching ahead of any obligation. This is addressed in full in Section 6.

→ One notable reversal: the European Commission’s proposed Green Claims Directive, which would have required formal substantiation of environmental claims including those referencing renewable electricity, was suspended following the Commission’s announcement of its intention to withdraw in June 2025⁷. However, the Empowering Consumers for the Green Transition (ECGT) Directive entered into force in March 2024, with member states required to transpose it by 27 March 2026⁸. The ECGT prohibits unsubstantiated environmental claims and explicitly covers renewable energy certificate-backed statements. The practical evidentiary standard for public GO-backed claims remains in place; only the legislative vehicle through which it would have been further codified has changed.

1.2 Rising Stakeholder Expectations

Regulatory compliance establishes a floor – it determines whether a company has disclosed correctly and met its legal obligations. But the stakeholders that materially affect a company’s cost of capital, customer relationships and financing access – institutional investors, large corporate buyers and sustainability-linked lenders – apply a second layer of criteria that goes beyond that floor. Those criteria are expressed through three voluntary frameworks: Carbon Disclosure Project (CDP), the Science Based Targets initiative (SBTi), and RE100. Each has tightened its electricity procurement quality bar in the past two years, and their collective direction of travel is unambiguous: away from annual average certificate matching, toward geographic specificity, asset additionality and temporal granularity.

Carbon Disclosure Project (CDP)

CDP’s annual disclosure platform aggregates sustainability data for institutional investors managing trillions in assets. Its scoring methodology now requires full third-party verification of Scope 1 and Scope 2 emissions as a baseline condition for Leadership-level scoring, with 100% coverage required for A List status. CDP explicitly distinguishes between high-integrity GO procurement – geographically matched, sourced from credibly new assets, with verified cancellation records – and low-integrity unbundled certificate purchases. A company that meets the technical minimum of the GHG Protocol market-based method by retiring cheap, legacy-asset GOs from a geographically distant market will score materially lower than one whose procurement meets additionality and matching criteria. That score feeds directly into institutional investor ESG assessments and, increasingly, into procurement qualification processes for large corporate customers.

The Science Based Targets initiative (SBTi)

Over 13,000 companies have committed globally to SBTi-aligned targets⁹. In November 2025, SBTi published an updated draft of its Corporate Net-Zero Standard V2 for public consultation, introducing a proposed “near, now, and new” framework for electricity procurement10:

- “New” – Generating facilities must have been commissioned or repowered within the past ten years, tightening to five years by 2035.

- “Near” – Procurement must be geographically matched to the same grid region as consumption

- “Now” – Hourly matching is required from 2030 at 50%, rising to 90% by 2040

Companies with existing SBTi commitments are therefore managing toward a procurement standard that tightens at defined intervals throughout their target period.

RE100

Previously, RE100 placed no formal age restriction on eligible generating facilities – assets of any age qualified toward a member’s renewable electricity claim. The October 2022 criteria first introduced a 15-year commissioning or re-powering limit, effective 2024; the 2025 update refined exemptions for long-term project-specific agreements, requiring at least 85% of a member’s renewable electricity to come from assets built or repowered within that window11. For the 442 RE100 members collectively consuming over 582 TWh annually, this directly caps the contribution of legacy hydro and wind assets – historically the primary source of cheap unbundled GOs in European markets – to no more than 15% of any renewable electricity claim¹². Geographic matching requirements further specify that electricity must be sourced within the same defined market boundaries as the consumption it is attributed to.

The combined effect of these three frameworks is clear: annual average matching from legacy assets, which for years represented the default procurement approach for many European corporates, now fails the quality criteria of every major voluntary standard simultaneously – and if SBTi’s proposed revisions are finalised as drafted, those requirements will tighten further at defined intervals. Companies whose procurement does not meet these criteria risk failing customer tender qualification requirements, receiving lower scores in investor ESG assessments, attracting assurance findings where public framework commitments cannot be evidenced, and losing access to sustainability-linked financing that references RE100 or SBTi alignment as covenant conditions.

1.3 Market Complexity Deepening

The European renewable electricity market has become structurally more complex to navigate at the same time as the standards for navigating it have tightened. Each dimension is addressed in turn below.

(1) Fragmentation across national registries with inconsistent evidentiary standards

The European GO market has always been fragmented but the degree of fragmentation and its consequences for buyers have increased.

Europe operates more than 30 national GO registries, each governed by its own issuing body, operating under varying interpretations of the EECS (European Energy Certificate System) framework and subject to different national transposition of RED III¹³. Cross-border GO transfers are technically possible within the EECS system but procedurally inconsistent: the standards for issuance metadata, vintage periods and cancellation documentation vary enough across jurisdictions that a GO cancelled in one registry may not carry the evidentiary weight expected by an auditor assessing a disclosure under a different national framework. For buyers procuring across multiple European markets, or consolidating multinational procurement, this means that GO quality cannot be assumed uniform; it must be verified at the registry and transaction level.

(2) Growing divergence between headline GO availability and the subset of certificates that meet current quality criteria

GO issuance volumes have grown faster than new renewable generation capacity in several European markets, reflecting the continued eligibility of legacy hydro and wind assets under pre-2025 frameworks. The result is a certificate market that has, at times, appeared well-supplied while the underlying generating assets are decades old, geographically concentrated and increasingly ineligible under the tightening voluntary framework criteria described in Section 1.2. That divergence between headline GO availability and the subset of certificates that actually meet quality criteria is what has driven price stratification in the market (examined further in Section 4).

(3) Surging demand from hyperscale data centres and semiconductor manufacturers compressing supply in key markets

The hyperscale data centre buildout across Europe – driven by AI infrastructure investment by Microsoft, Google, Amazon and others – has created sustained, large-volume demand for high-quality, geographically and temporally matched renewable energy. These buyers are not marginal participants: they are procuring at scale, with long-term PPA structures, and their procurement criteria directly set the quality benchmark that the rest of the market is now measured against. The semiconductor manufacturing expansion, particularly in Germany, the Netherlands and Ireland, adds further baseload renewable demand in markets with already-constrained high-quality GO supply.

(4) Multinationals with APAC operations and the challenge of consolidating GO and I-REC procurement into a single auditable Scope 2 framework

For European multinationals with significant APAC operations, a fourth layer of complexity applies. Scope 2 reporting under CSRD operates on a consolidated basis. A single market-based Scope 2 figure must represent all entities in scope, including those consuming electricity in markets where GOs do not exist. Across most of APAC, the applicable instrument is the I-REC Standard certificate, which operates under a different governance structure, different registry infrastructure, and different quality tiers than the European GO system. Building a single, coherent Scope 2 governance framework that spans both systems – with consistent evidence chains, auditor-ready documentation, and procurement criteria that satisfy both ESRS E1-6 and major voluntary framework requirements – is a materially different exercise than managing a single-market GO programme. The practical implications for APAC procurement are addressed in Section 2.5.

Taken together, these three forces – tightening regulation, rising stakeholder expectations and deepening market complexity – have fundamentally changed the nature of Scope 2 procurement. What was once a low-scrutiny, internally managed sustainability metric is now an externally assured disclosure obligation, an integrity-differentiated market position, and an operationally complex procurement challenge. The rest of this guide addresses each dimension in turn: what the GO instrument is and how it works (Sections 2 and 3), how to procure at the quality level the market now requires (Sections 4 to 6), and how to manage residual emissions and build a long-term strategy (Sections 7 and 8).

2. Foundations: Understanding Scope 2 and Guarantees of Origins (GOs)

This section establishes the methodological and instrument foundations that all subsequent sections build upon. Readers already familiar with the GHG Protocol Scope 2 Guidance and GO mechanics may proceed to Section 3.

2.1 Scope 2 Accounting Methods and Certificate Terminology

Scope 2 emissions are the indirect greenhouse gas emissions associated with purchased electricity, heat, steam and cooling. They are indirect because the emissions occur at the point of generation, not within the company’s own operations. However, they are attributed to the consuming organisation because its consumption drives the generation. For most European corporates, purchased electricity is the dominant Scope 2 component, and it is the component the GO framework addresses. Purchased heat and cooling are outside the scope of this guide.

The methodological foundation for Scope 2 accounting globally is the GHG Protocol Scope 2 Guidance, published in 2015¹. Although it is not EU law, but a privately developed voluntary standard, CSRD’s ESRS E1-6 is explicitly built upon it. When ESRS E1-6 mandates dual reporting of location-based and market-based Scope 2 figures, it is mandating the two methods the GHG Protocol defines.

- Location-based method calculates Scope 2 based on the carbon intensity of the grid your facility is connected to, applied to total electricity consumed. It reflects physical grid reality: your certificates and contracts do not affect this figure. A factory in Poland and a factory in France consuming identical amounts of electricity will report very different location-based Scope 2 figures, because their grids have different carbon intensities.

- Market-based method calculates Scope 2 based on the contractual instruments you hold. If you hold no instruments, the residual mix factor applies – the emission factor representing what remains of the grid’s generation pool after all renewable attributes have been claimed by EAC buyers. Because the cleanest generation has already been allocated, the residual mix is almost always dirtier than the national grid average. This is why two companies on the same grid can report very different market-based Scope 2 figures – one has procured certificates, the other has not.

Both figures are mandatory under ESRS E1-6. The gap between them is itself a disclosure – auditors and investors will read it as an indicator of how much a company’s reported Scope 2 position depends on certificate procurement rather than physical grid decarbonisation.

Certificate terminology

The renewable electricity certificate market operates under several overlapping terms, and precision matters – particularly for CSRD audit documentation where instrument type must be correctly identified. Energy Attribute Certificates (EACs) is the umbrella term for all renewable electricity certificates globally – GOs, RECs and their equivalents in other markets are all EACs.

- Guarantees of Origin (GOs) are the EU-mandated EAC instrument, established under the Renewable Energy Directive and governed by the Association of Issuing Bodies (AIB) across Europe and the European Economic Area (EEA). When this guide refers to certificate procurement in European markets, GOs are the applicable instrument unless otherwise specified.

- Renewable Energy Certificates (RECs) are used across North America and Asia, and widely adopted as a generic global term for renewable electricity certificates. In APAC, most RECs are issued under the I-REC Standard (explained in full in Section 2.5). Using REC terminology in CSRD documentation where a GO cancellation record is required would be an evidentiary mismatch.

- Other domestic instruments. Several markets operate certificate frameworks outside both the AIB and I-REC systems, including China’s Green Electricity Certificate (GEC), Japan’s Non-Fossil Certificate (NFC), South Korea’s K-REC, India’s REC under CERC and Turkey’s YEK-G renewable electricity certificate system. For multinationals with operations in these markets, the applicable instrument and its CSRD evidentiary requirements differ from GOs. These are addressed in Section 2.5.

GOs are a statutory instrument established under the EU Renewable Energy Directive. Issuance is mandatory – a GO must be issued for every MWh of eligible renewable electricity generated, which means supply is directly tied to actual renewable generation rather than market demand.

The AIB and the EECS

The operational governance of the GO system sits with the Association of Issuing Bodies (AIB), a non-profit organisation that administers the European Energy Certificate System (EECS) – the rulebook governing how GOs are issued, transferred, cancelled and disclosed across its member registries. AIB membership currently covers 25 countries across Europe and the EEA¹³. National registries operate under their own issuing bodies but must comply with EECS rules to participate in cross-border transfers via the AIB Hub, the infrastructure connecting national registries. In Europe, AIB‑issued Guarantees of Origin are the most widely accepted instruments for market‑based Scope 2 reporting under CSRD, but non‑AIB GOs may still qualify if they meet GHG Protocol quality and evidence requirements.

National instruments

While the GO is the EU-mandated instrument, national implementation varies. For example:

- Germany: Herkunftsnachweise (HKN), administered by the Umweltbundesamt (UBA).

- United Kingdom (UK): Renewable Energy Guarantees of Origin (REGOs), administered by Ofgem. The UK left the AIB framework following Brexit; REGOs are no longer transferable into EU registries via the AIB Hub, and their use in CSRD documentation requires specific auditor guidance on evidentiary validity.

- Nordics: Norway and Sweden operate Elcertifikat systems alongside GOs. Elcertifikats are a separate instrument and are not valid for CSRD market-based Scope 2 claims.

- Italy: Administered by Gestore dei Servizi Energetici (GSE).

- France: GOs are issued under the authority of the French state and operated by Powernext (EEX Group) by delegation from the French state.

- Spain: Administered by CNMC (Comisión Nacional de Mercados y la Competencia)14.

How a GO is created, transferred and cancelled

Issuance: 1 GO is issued for every 1 MWh of eligible renewable electricity generated, verified via production meter data. The GO record contains technology type, generation facility location, generation period and a unique certificate identifier.

Transfer: GOs can be sold and transferred within the same national registry or across borders via the AIB Hub. Each transfer is recorded; a GO can change hands multiple times before cancellation.

Cancellation: The legal act by which a corporate retires the GO against its electricity consumption. Once cancelled, it cannot be reused. The cancellation statement is the primary evidentiary document for a CSRD market-based Scope 2 claim and must show: number of GOs cancelled, generation period, technology type, country of origin and cancellation date.

Vintage rules. A GO is valid for cancellation within 12 months of the end of the generation period.

2.3 What a GO does and what it does not

| What a GO proves | What a GO does not prove |

|---|---|

| 1 MWh of electricity generated from a renewable source | Additionality: that the purchase financed new renewable capacity |

| Technology type (wind, solar, hydro, biomass, etc.) | Physical delivery: that renewable electrons reached your grid |

| Country and region of generation | Geographic matching: that generation occurred in your grid zone or price area |

| Generation period (month and year) | Temporal matching: that generation occurred when you consumed electricity |

| Exclusive claim: cancellation is one-time and irreversible | Asset quality: the age or carbon displacement value of the generating asset |

Additionality is the most debated limitation. A GO from a hydro plant built in 1970 is fully valid under EECS. The GO system was designed to track and attribute existing renewable generation, not to drive new capacity – which is precisely the gap that SBTi and RE100 additionality criteria are designed to close.

Physical delivery is the most publicly misunderstood. A GO cancelled in Germany from Norwegian hydro does not mean those electrons reached Germany. The GO certifies the attribute, not the electron – and this distinction is where most NGO and media criticism of corporate renewable claims is anchored.

Geographic and temporal matching are where requirements are heading. CSRD requires neither, which in European practice has typically meant annual cancellation of GOs from the AIB area against consumption in any member state. SBTi, RE100 and CDP all apply geographic criteria, and hourly matching is the direction voluntary frameworks are moving in, addressed in Section 6. The result: a GO that is valid under CSRD may simultaneously fail all three voluntary framework criteria.

2.4 The instrument landscape: when each one fits

Different instruments serve different procurement objectives. For CSRD market-based reporting, GOs are the core instrument because they are the recognised certificate type for European Scope 2 claims. For broader credibility goals such as additionality, geographic alignment, or long-term decarbonisation signalling, companies may layer GOs with other instruments like PPAs or utility green tariffs.

GO procurement. GOs are the standard instrument for market-based Scope 2 in Europe. They are liquid, standardised, widely available across the AIB system, and relatively easy to procure and cancel at scale. That makes them the practical default for companies that need a compliant, auditable and operationally manageable solution.

Corporate long-term Power Purchase Agreements (PPAs) are usually chosen by companies that want a more direct relationship with generation and, in some cases, new renewable capacity. They can support additionality claims where the project is new-build, but they require volume, credit strength and long-term commitment that many corporates do not have. More in detail under Section 4.4.

Utility green tariffs sit between spot certificates and bespoke PPAs. They are operationally convenient and can simplify procurement across distributed sites, but their underlying quality depends on how the tariff is structured and whether it is backed by specific generation or a broader pool. More in detail under Section 4.5.

Most companies do not use one instrument alone. A common approach is to use PPAs or green tariffs for part of the load and GOs for residual consumption, ensuring both operational practicality and compliant market-based reporting. The key point is not that one instrument replaces another, but that each plays a different role in the overall procurement mix.

2.5 RECs in Asia-Pacific: Implications for multinational Scope 2 consolidation

For multinational corporates consolidating Scope 2 disclosures under a single reporting framework, APAC introduces a second certificate environment alongside Europe’s GO system. The accounting logic established in Section 2.1 remains the same – location-based and market-based methods under GHG Protocol Scope 2 Guidance – but the applicable instruments, issuers and evidentiary requirements differ materially by market.

APAC operates a mix of I-REC markets and domestic certificate regimes. The International Renewable Energy Certificate (I-REC) is the dominant instrument across Singapore, Malaysia, Indonesia, Thailand, Philippines, Vietnam, Japan, South Korea, India and other markets where no equivalent national system exists.

Key APAC certificate markets

- I-REC markets: Singapore, Thailand, Philippines, Vietnam, Taiwan, Hong Kong

- Domestic systems: China (GECs), Japan (NFCs), Australia (LGCs)

- Hybrid markets: Indonesia, Malaysia, India, South Korea

I-RECs follow the same issuance-transfer-cancellation flow as GOs but use Evident registry instead of AIB systems. Unlike GOs, which expire after 12 months, I-RECs do not formally expire.

Reporting, limitations and CSRD consolidation

APAC EAC demand is surging, driven by RE100 commitments, national net-zero pledges and ASEAN’s own regional renewable energy targets15. However, APAC markets remain less mature than Europe’s AIB system, with thinner liquidity, lower additionality scrutiny, limited residual mix data16, and less standardised vintage rules across registries. I-RECs receive identical GHG Protocol Scope 2 treatment as GOs, supporting market-based claims when retired under the same SBTi/RE100/CDP quality criteria.

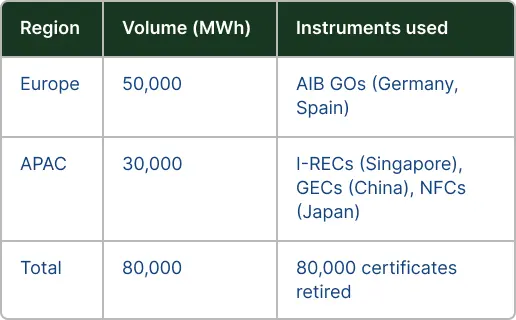

When consolidating Scope 2 across Europe and APAC, auditors expect GO cancellation statements from AIB registries for European consumption, and I-REC or local certificate retirement records for APAC operations. Group sustainability teams typically map consumption by market, procure the applicable local instruments and generate retirement evidence from the relevant registry – Evident for I-RECs, APX for TIGRs, and local registries where applicable. Uniform market-based accounting can then be applied across regions under a single CSRD E1-6 methodology. Certificate procurement becomes a group-level reporting requirement.

Example consolidated disclosure:

Market-based Scope 2 Coverage by Region

3. CSRD and ESRS E1: Disclosure Requirements and Audit Readiness

ESRS E1 is one of ten topical standards within the European Sustainability Reporting Standards framework. To understand what E1 requires and why its disclosure obligations are structured the way they are, it helps to understand where it sits within the broader ESRS architecture.

The ESRS framework is organised into two levels:

1. Cross-cutting standards – two standards that apply across all sustainability topics:

- ESRS 1 – General Requirements: governs how companies apply the ESRS framework, including materiality assessment, reporting boundaries and the structure of sustainability statements

- ESRS 2 – General Disclosures: requires disclosure of governance, strategy, impacts/risks/opportunities, and metrics and targets applicable to all sustainability topics

2. Topical standards – ten standards covering specific sustainability topics, organised under three pillars:

For most companies in scope, ESRS E1 is the topical standard with the most direct operational implications for their renewable electricity procurement decisions. Its nine disclosure requirements (E1-1 through E1-9) cover the full spectrum of climate-related disclosures, from transition planning and energy consumption through to GHG emissions, carbon credits, and physical and transition risk financial effects.

3.1 The full ESRS E1 Climate Change structure

Although each of ESRS E1’s nine disclosure requirements addresses a distinct topic, auditors read them together: the renewable electricity volumes reported under E1-5 must reconcile with the market-based Scope 2 figure reported under E1-6, and the carbon credits disclosed under E1-7 must be clearly separate from the GO procurement that supports the E1-6 market-based claim. An inconsistency across any of the three will be identified under assurance. The nine disclosure requirements within ESRS E1 are structured as follows:

| Disclosure | Title | Relevance to GO procurement |

|---|---|---|

| E1-1 | Transition plan | GO strategy must connect to documented decarbonisation pathway |

| E1-2 | Climate policies | Renewable electricity policy and procurement commitments |

| E1-3 | Actions and resources | Procurement budget, PPA commitments, GO programme scope |

| E1-4 | Targets | Scope 2 absolute reduction targets and base year logic |

| E1-5 | Energy consumption and mix | GO cancellation records are the direct evidence base |

| E1-6 | GHG emissions | Dual Scope 2 reporting = location-based + market-based |

| E1-7 | Carbon credits and removals | Must not be conflated with GO/REC strategy |

| E1-8 | Physical risk financial effects | Indirect relevance – procurement geography concentration |

| E1-9 | Transition risk financial effects | Indirect relevance – regulatory and market exposure |

E1-1 through E1-4: Strategy, policies, actions and targets

These disclosures address how a company has embedded climate change into its governance and strategic planning. E1-1 covers the transition plan and decarbonisation pathway – where GO procurement connects to a company’s broader climate strategy. For example, a company that reports a Scope 2 reduction under E1-6 must be able to support it with a documented procurement approach under E1-1. E1-3 requires disclosure of actions and resources allocated, which includes procurement budget commitments and any PPA structures. E1-4 addresses targets, including Scope 2 absolute reduction targets and the base year logic against which progress is measured.

E1-5: Energy consumption and mix

E1-5 requires disclosure of total energy consumption split between renewable and non-renewable sources. GO cancellation records are the direct evidence base for any renewable electricity claim made here. Addressed in depth in Section 3.2.

E1-6: Gross Scope 1, 2 and 3 GHG emissions

E1-6 covers gross GHG emissions across all three scopes, with Scope 2 requiring dual reporting under both the location-based and market-based methods. The market-based figure is the one directly affected by GO procurement decisions. Addressed in depth in Section 3.2.

E1-7: Carbon credits and removals

E1-7 requires separate disclosure of carbon credits purchased and carbon removals claimed. GOs and carbon credits are distinct environmental instruments operating under different frameworks and serving different disclosure requirements: GOs address the source of energy consumed while carbon credits address residual emissions not yet reduced. This distinction is addressed further in Section 7.2.

E1-8 and E1-9: Physical and transition risk financial effects

These disclosures address the financial materiality of climate-related physical and transition risks respectively. A company whose renewable procurement strategy is concentrated in a single geography or technology may have transition risk exposure relevant to E1-9, but these disclosures are outside the direct scope of this guide.

3.2 E1-5 and E1-6 in depth: where your certificates become your evidence

E1-5 and E1-6 are the two disclosure requirements where renewable electricity procurement decisions have the most direct and auditable impact on a company’s sustainability statement.

E1-5: Energy Consumption and Mix

E1-5 requires companies to disclose total energy consumption in megawatt-hours (MWh), broken down across three source categories:

- Fossil sources: total consumption from fossil fuels

- Nuclear sources: reported separately, not grouped with renewables

- Renewable sources: disaggregated into three sub-categories:

- Fuel consumption from renewable sources (biomass, biogas, renewable hydrogen, etc.)

- Purchased or acquired electricity, heat, steam and cooling from renewable sources

- Self-generated non-fuel renewable energy

Where a company also produces energy on-site, it must separately disclose that production volume in MWh for both renewable and non-renewable sources.

The GO and REC provision – ESRS E1, AR 32(j)

This is the most important rule in E1-5 for any renewable electricity buyer. A company may only classify purchased electricity as renewable if the contractual arrangement clearly identifies its origin – through a PPA, a standardised green tariff, or a market instrument such as a Guarantee of Origin (GO) in Europe or a Renewable Energy Certificate (REC) in Asia or North America17. Without one of these instruments, the electricity must be reported as non-renewable, regardless of what the supplier’s tariff is called.

Additional requirement for high climate impact sectors

Companies with operations in high climate impact sectors (defined under NACE Sections A to H and Section L, covering agriculture, mining, manufacturing, energy, construction, transport, hospitality and real estate) must also break down their total fossil fuel consumption into17:

- Coal and coal products

- Crude oil and petroleum products

- Natural gas

- Other fossil fuels

- Purchased electricity, heat, steam, or cooling from fossil sources

The requirement is triggered if any part of your business falls under those NACE sections. Once triggered, the breakdown must cover your entire company – every division and operation, not just the ones in those sectors. Companies in these sectors must also report an energy intensity ratio: total energy consumption (MWh) divided by net revenue (EUR), calculated only from the high climate impact activities, with the net revenue figure reconciled to the financial statements.

Common errors in E1-5 reporting

1. Timing mismatch: GOs or RECs must be cancelled within the reporting period, or where cancellation occurs after year-end, the cancellation statement must explicitly reference the prior consumption year and precede audit sign-off. Certificates cancelled after audit sign-off cannot support the prior year’s renewable claim.

- Example: A company consumes electricity in December 2024 and cancels the corresponding GOs in February 2025, before audit fieldwork begins in March 2025, with the cancellation statement referencing the 2024 consumption year. This is acceptable. If the same cancellation occurred after audit sign-off, it could not support the 2024 claim.

2. Geographic mismatch: under stricter interpretations and emerging best practice (addressed in Section 5), GOs and RECs should correspond to electricity from the same market zone as the consumption site.

- Example: Norwegian hydropower GOs cancelled against consumption at offices in the Czech Republic do not reflect the electricity actually available on the Czech grid.

3. Volume mismatch: partial coverage must be disclosed as such; a company that covers 60% of its consumption with GOs or RECs cannot report 100% renewable electricity

- Example: Out of 10,000 MWh consumed annually, only 6,000 MWh is covered by GOs or RECs; the company must report 60% renewable electricity, not 100%.

E1-6: Gross Scope 1, 2, 3, and Total GHG Emissions

E1-6 requires companies to report gross greenhouse gas emissions in metric tonnes of CO2 equivalent (tCO2e). Gross means before any netting against carbon credits or removals (those are reported separately under E1-7). The four required figures are:

- Gross Scope 1 GHG emissions

- Gross Scope 2 GHG emissions

- Gross Scope 3 GHG emissions

- Total GHG emissions (sum of all three)

Scope 1: direct emissions

Scope 1 covers direct emissions from sources the company owns or controls – stationary combustion, mobile combustion, process emissions and fugitive emissions. The total gross figure must be disclosed in tCO2e, along with the percentage covered by regulated emission trading schemes such as the EU ETS. Biogenic CO2 from biomass combustion is disclosed separately and does not enter the Scope 1 total, though other GHGs from biomass (CH4, N2O) are included.

Scope 2: dual reporting

Scope 2 must be reported under both the location-based and market-based methods, as defined in Section 2.1. A company cannot report only the market-based figure. As a quick reference:

| Method | What it matters | Key input |

|---|---|---|

| Location-based | Grid carbon intensity × consumption | National or residual mix emission factors |

| Market-based | Carbon intensity of contractually sourced electricity | GO/REC cancellation statements; PPA terms |

The market-based figure is reduced through GO and REC procurement. When a GO or REC is cancelled against consumption, the emission factor for that electricity drops to zero.

The residual mix is the emission factor assigned to electricity that has no renewable certificate attached to it. Because every GO or REC buyer has already claimed the clean generation on the grid, what is left tends to be significantly dirtier than the headline grid average. In most European markets, this means an uncovered company’s market-based Scope 2 figure ends up higher than its location-based figure, not lower.

Under ESRS E1 (AR 45), companies must disclose the share and types of contractual instruments used to support the market-based figure – including GOs and RECs17. This is the direct disclosure hook connecting E1-6 to a company’s renewable electricity procurement programme.

Scope 1 and Scope 2 figures must be broken down separately between the company’s own consolidated group and any partially owned entities (joint ventures or associate companies) where the company has operational control.

Scope 3: value chain emissions

Companies must report emissions from each significant Scope 3 category – those identified as material following a screening of all 15 GHG Protocol categories. They must state which categories are included, which are excluded, and why. Phase-in provisions apply: companies with fewer than 750 employees may omit Scope 3 in their first reporting year.

Scope 3 sits outside the direct scope of this guide, but context matters: for most corporate buyers, Scope 3 Category 1 (purchased goods and services) and Category 11 (use of sold products) are typically far larger than Scope 1 and 2 combined, which is why a strong Scope 2 market-based position, however well-evidenced, is rarely sufficient as a standalone climate strategy.

Total GHG emissions and intensity

Once all three scopes are reported, two further disclosures are required at the total emissions level:

- Total GHG emissions reported twice – once incorporating the location-based Scope 2 figure and once incorporating the market-based figure. This allows auditors and investors to see how much of the difference between the two totals is driven by certificate procurement.

- A GHG intensity ratio – total emissions divided by net revenue – required for both versions. The net revenue figure used must match what appears in the company’s audited financial statements; it cannot be adjusted or restated for this purpose.

3.3 Audit Readiness for Scope 2 and GO Claims

The three common errors covered in Section 3.2 – timing, geography and volume mismatches – are the most frequently cited findings under assurance. But knowing the rules and being able to demonstrate compliance to an auditor are two different things. This section is about the latter.

What auditors are actually checking

A GO has a documented lifecycle: it is issued by a national registry at the point of generation, transferred through the market, and cancelled in the buyer’s name against a specific consumption period. Auditors refer to this sequence as the chain of custody and their job under limited assurance is to test whether your documentation can prove each link in that chain is intact. That means working backwards from your E1-5 and E1-6 disclosures to the underlying registry records. For every MWh you report as renewable, they will ask: is there a cancelled certificate that corresponds to it, and can you prove it?

The Evidence Hierarchy

The chain of custody is only as strong as the documentation behind it. Auditors expect three layers, each serving a purpose the previous one cannot:

| Layer | Document | Role |

|---|---|---|

| 1 – Primary | GO/REC cancellation statement from the national registry | Proves cancellation occurred and names your entity as beneficiary |

| 2 – Corroborating | Registry export: serial numbers, technology, vintage, cancellation date | Independent verification; cannot be issued or modified by the seller |

| 3 – Commercial | Purchase contract, invoice, attribute specification | Connects the transaction to the cancellation and demonstrates your procurement criteria were applied |

A broker confirmation and an invoice however detailed, sit entirely within Layer 3. Without Layers 1 and 2, they are not audit-ready evidence of a renewable claim.

Example: A company reports 10,000 MWh of renewable electricity under E1-5. Its cancellation statement covers 8,000 MWh in its own name; the remaining 2,000 MWh is covered by a broker confirmation that does not reference a registry cancellation. The 2,000 MWh claim cannot be substantiated and must either be re-evidenced or removed from the renewable total.

Pre-Audit Documentation Checklist

How you procure directly determines whether this checklist can be satisfied. Section 5 covers the procurement structures, contract terms and cancellation mechanics that make this evidence chain possible.

| Item | What to verify |

|---|---|

| Beneficiary name | Cancellation statement names your legal entity, not a broker or parent company |

| Registry corroboration | Serial numbers, technology, vintage and cancellation date visible in a registry-level export |

| Chain of title | Transfer records from issuer through any intermediary to your entity are unbroken |

| Volume reconciliation | MWh of certificates cancelled reconciles to metered consumption at site level |

| Geographic alignment | Country of generation matches country of consumption, or cross-border transfer is documented |

| Timing | Cancellation date falls within the reporting period or explicitly references the prior consumption year and precedes audit sign-off |

| Entity mapping | Every legal entity in your CSRD reporting boundary has its own cancellation documentation |

| Vintage compliance | Generation year meets applicable framework requirements (e.g. RE100’s 15-year rule) |

| Partial coverage | Any uncovered volume is disclosed and reported at the correct residual mix factor |

How you procure directly determines whether this checklist can be satisfied. Section 5 covers the procurement structures, contract terms and cancellation mechanics that make this evidence chain possible.

4. Understanding the European GO Market

The European GO market is not a single, homogeneous pool of interchangeable certificates. It is a collection of national markets – each with its own registry, supply dynamics and pricing. A GO from a Norwegian hydro plant and a GO from a Spanish solar facility are legally equivalent under the EECS framework, but they are not commercially equivalent, they are not equally credible under voluntary frameworks, and they do not carry the same evidentiary weight in every audit context. Understanding those distinctions and building a procurement programme that accounts for them is the substance of this section.

4.1 Market Fragmentation: Country-by-Country Reality

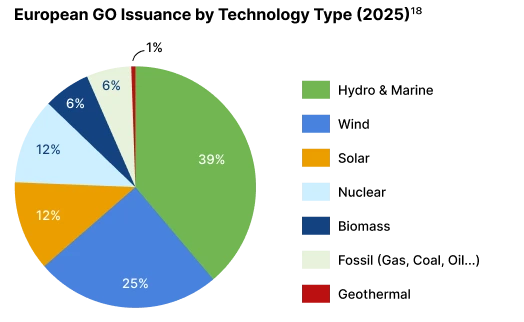

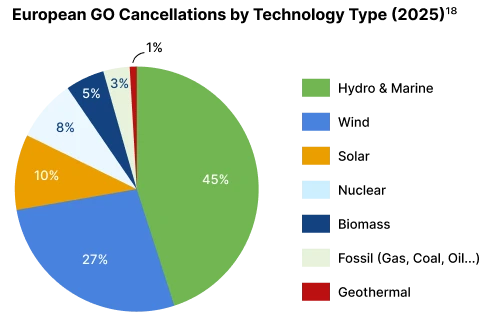

As expressed in Section 1.3 earlier, the European GO market spans more than 30 national registries, all operating under the EECS framework but with material differences in how they function. The 2025 AIB data makes this fragmentation concrete: Norway alone accounted for 14.4% of all European electricity GO issuances, while Germany – the continent’s largest economy and electricity consumer – issued just 4.2% of total supply but absorbed 20.5% of all cancellations18. That gap between where GOs are produced and where they are consumed is the defining structural feature of the market, and it plays out differently in every country.

The technology mix behind these flows is equally uneven: hydro and marine sources accounted for 39% of GO issuances in 2025 but 45% of cancellations — a gap that reflects where renewable generation is concentrated across the continent.

| Supply concentration in the north Norway is the single largest source of European GOs, issuing 156.7 TWh in 2025 with a supply-to-demand ratio of 5.1. This means they produce roughly five certificates for every one cancelled domestically. Over 91% of Norwegian issuances are hydro-based. Iceland sits at a ratio of 2.4. Both are structural exporters, and their surplus keeps Nordic hydro at the lower end of the market. For buyers, the implication is straightforward: volume is available, but it comes predominantly from legacy hydro assets that do not meet the additionality criteria required by RE100, SBTi, or similar voluntary frameworks. |

| The Netherlands: disclosure rules, constrained supply The Netherlands has introduced comprehensive disclosure requirements that have driven strong local demand for GOs, creating price pressure on geographically matched certificates that buyers in other markets don’t face to the same degree. In 2025 the country sat just below balance – 102.8 TWh issued against 114.9 TWh cancelled – but that ratio overstates available renewable supply. Over a third of Dutch issuances came from fossil natural gas, with hard coal adding a further 8%. Wind and solar dominate the renewable portion, but for any buyer with a technology requirement, the effective local pool is considerably tighter than the headline figure suggests, and 81.5 TWh had to be imported to fill the gap. |

| Germany: supply-demand mismatch Germany’s position is unlike any other market in the system. In 2025, it cancelled 223.9 TWh – more than any other country – while issuing only 46.0 TWh, a supply-to-demand ratio of 0.21. This structural shortfall has a regulatory cause: German renewable generators receiving state support are not permitted to issue GOs for their output, capping local supply well below domestic demand. Germany imported 217.8 TWh in 2025 to partially bridge the gap, making it by far the largest net importer in the system. Buyers seeking GOs that correspond geographically to German consumption must either accept imported certificates – creating a country-of-origin mismatch – or procure through PPAs or green tariffs that bundle local generation with GO issuance. |

| Southern Europe: where quality supply is growing Spain, Portugal, France and Italy collectively represent the most attractive sourcing region for buyers with technology and vintage requirements. Spain’s mix is now 56% solar and 32% wind – newer assets, better additionality credentials – with a supply-to-demand ratio of 3.7, meaning meaningful export capacity exists. Portugal and France follow similar profiles. Italy has moved close to balance but offers a diversified mix across hydro, solar, wind and biomass. For buyers who need to demonstrate RE100 or SBTi commitments, this is the part of the market worth watching and increasingly worth paying a premium for. |

Under the market-based method, any AIB-issued GO satisfies CSRD regardless of where the electricity was consumed. Geography, technology and vintage are not regulatory requirements, but they are increasingly what assurance providers, RE100, SBTi and CDP are looking for. A certificate that clears the regulatory bar and nothing else is a liability, not an asset.

How cross-border GO transfers work

The AIB Hub connects national registries and enables GO transfers across EECS member countries. Transfers are only possible where bilateral or multilateral agreements exist between registries, and some impose timing restrictions or additional requirements on incoming certificates. Availability depends on which registry your counterparty operates in and whether a transfer pathway exists.

4.2 Technology and vintage: why not all GOs are equal

As covered in Section 2.3, a GO proves that 1 MWh was generated from a renewable source but does not prove the age of the generating asset or whether its construction was financed by the certificate purchase. Technology type and vintage are the two attributes where voluntary frameworks create differentiation.

Technology

Wind and solar GOs are generally preferred over hydro by buyers seeking to demonstrate additionality. Hydro generation is largely from long-established assets; wind and solar procurement is more likely to correspond to capacity built in the past decade. This preference is reflected in pricing. Solar GOs from recently commissioned assets are the fastest-growing segment of the GO market, with the highestgrowth rate between 2019 and 2023 and anticipated to remain so through 203418.

Biomass and biogas GOs are valid under EECS but carry additional credibility risks: their sustainability depends on feedstock sourcing, which is subject to separate certification requirements under RED III. For CSRD reporting, biomass electricity classified as renewable must meet the sustainability criteria under RED III Article 295. Buyers should verify these criteria are met before including biomass GOs in their evidence package.

Vintage

Vintage refers to the year in which the electricity was generated, not the year of cancellation. Under EECS rules, a GO is valid for cancellation for 12 months after the end of the generation period. Under RE100’s 2025 criteria, the generating asset must have been commissioned or repowered within the past 15 years. Under SBTi’s updated framework, generating assets must be within 10 years of commissioning as of 2025, tightening to 5 years by 2035.

This creates a practical planning horizon. For example, GOs procured today from assets commissioned in 2010 will fall outside SBTi’s 10-year window in 2030. Procurement teams building multi-year strategies need to account for rolling asset eligibility, not just current compliance.

4.3 GO price dynamics

GO prices are set by supply and demand across the AIB system, shaped by the forward market and the attribute specifications buyers require.

| Supply | Demand | |

|---|---|---|

| Key drivers | One GO is issued per eligible MWh of renewable generation, so supply moves directly with weather, hydro reservoir levels, wind output and new capacity build-out. | • CSRD is the most significant new structural demand driver. Wave 1 companies (large EU public-interest entities, FY2024) began purchasing under audit-facing conditions in 2024 and 2025. • RE100, SBTi and CDP commitments layer additional demand on top, concentrated in higher-quality certificates. |

| Structural trend | • AIB members surpassed 1,000 TWh of EECS electricity GOs issued in 2024 (a 10% increase YoY) with cancellations growing 12% to 884 TWh. • Total issuance volumes are high and rising, but effective supply for quality-seeking buyers is narrowing as RE100 and SBTi asset age thresholds exclude an increasing share of legacy hydro from qualifying procurement pools. | The Omnibus I Directive delays CSRD application deadline for Wave 2 and Wave 3 companies. This has introduced near-term demand uncertainty. Wave 1 obligations remain in force, and voluntary framework commitments continue to drive purchasing independently of CSRD timelines. |

Price context

The GO market has historically been characterised by significant price volatility, with supply-side shocks –particularly drought-driven hydro shortages – capable of moving prices sharply within a single year. The structural oversupply that depressed prices through 2023 and 2024 was driven by strong renewable capacity additions outpacing demand growth, not by lack of market interest. AIB data confirms this: cancellations grew 12% in 2024 to 884 TWh, reflecting sustained and growing use of GOs for consumption disclosure even as prices fell18.

The market is now in a transitional period. Oversupply persists at the headline level, but effective supply for quality-seeking buyers is narrowing as voluntary framework criteria tighten. On the demand side, the Omnibus Directive delayed CSRD application for Wave 2 and Wave 3 companies, introducing near-term uncertainty. Wave 1 obligations remain in force, and voluntary commitments continue to drive purchasing independently of CSRD timelines. Wood Mackenzie market analysis of March 2026 found that, under base case assumptions, GO prices are expected to remain moderate through the medium term19.

Buyers should treat current price conditions as a procurement window rather than a permanent baseline. The combination of tightening quality criteria, expanding reporting obligations, and a maturing forward market points toward a structurally different supply-demand balance over the next five years.

As of early 2025, forward contract prices for GOs were sitting above spot prices. This signals that the market expects certificates to become more expensive as CSRD-driven demand builds and qualifying supply tightens. For corporate buyers, this is a practical prompt: buying now, or locking in forward contracts, is likely cheaper than waiting.

4.4 GOs under scrutiny: separating legitimate criticism from unfounded dismissal

The debate around GO credibility has intensified as corporate climate commitments have multiplied and scrutiny of renewable energy claims has grown. NGO campaigns, investigative journalism, and academic research have questioned whether GO-backed “100% renewable” claims are meaningful. For a procurement team building a serious programme, that scrutiny deserves a direct answer.

Not all GO criticism targets the same thing. Some is directed at low-quality procurement – legacy assets, no geographic matching, claims that go beyond what the instrument supports. That criticism is fair, and it has had a visible effect on the market: the price stratification in Section 4.3, the growing premium for new-vintage and geographically matched certificates, and the tightening vintage criteria from RE100 and SBTi all reflect a market responding to legitimate pressure.

Some criticism is directed at the GO instrument itself, arguing it has no place in corporate climate accounting. That criticism conflates the instrument’s limitations with invalidity. As covered in Section 2.3, a GO does not claim to prove additionality, physical delivery, or temporal alignment – and within the accounting framework it operates in, it is not required to. Its job is to track and attribute the renewable attributes of generation to the buyer who cancels the certificate. It does that reliably, under a registry infrastructure specifically designed for that purpose.

The companies facing genuine reputational and legal exposure are those procuring cheap certificates while making claims that go beyond what those certificates support – particularly now that the ECGT sets a substantiation standard for consumer-facing renewable claims.

5. GO procurement strategy

Sections 1 through 4 have covered why Scope 2 procurement matters, how the GO instrument works, what your disclosure obligations require, and what the European market looks like. This section walks through the procurement process in sequence. By the end, you should have a clearer view of how to shape a procurement programme that aligns with CSRD, holds up against voluntary framework expectations, and is operationally manageable for your organisation’s size and structure.

5.1 Define Your Procurement Specification

Before approaching any supplier, broker or exchange, a buyer needs a clear internal specification. Without one, you cannot evaluate whether what you are being offered meets your needs, and you will not be able to demonstrate to an auditor that your procurement criteria were defined and applied consistently.

The specification has five components:

1. Volume. Total MWh of electricity consumed across all legal entities within your CSRD reporting boundary, by country. This is not your group’s headline energy figure – it is entity-level consumption, mapped to the registries where cancellations will need to occur. If your consumption data is not yet at entity level, resolving that gap is the first step before any procurement decision.

2. Geography. Which countries do your consuming entities operate in? This determines which national registries are relevant, whether cross-border transfers are required, and whether geographic matching under RE100 or SBTi is achievable within your consumption footprint. A buyer consuming in Germany faces a structurally different sourcing challenge than one consuming in Spain – as covered in Section 4.1.

3. Framework commitments. Are you procuring to satisfy CSRD only, or do you also need to meet RE100, SBTi, and/or CDP criteria? The answer directly determines your minimum quality floor. CSRD requires annual cancellation from any AIB-member registry – that is the legal minimum. RE100 adds a 15-year asset age requirement and national geographic matching. SBTi adds a 10-year asset window tightening to 5 years by 2035, and same-grid procurement. Designing to the most stringent applicable criterion across all three frameworks from the outset avoids a procurement rebuild later.

4. Quality specification. Based on your framework commitments, define the minimum attributes you will accept:

- Technology type (e.g. wind and solar only, or hydro included)

- Asset commissioning year (e.g. commissioned post-2010 for current SBTi alignment)

- Country of generation (e.g. same country as consumption, or cross-border accepted)

- Vintage (generation year must fall within your reporting period)

This specification becomes the attribute schedule in your procurement contract. A supplier who cannot confirm these attributes against the certificates they are offering cannot meet your specification.

5. Timeline. When must cancellations occur? Work backwards from your audit sign-off date. As established in Section 3.3, cancellations must either fall within the reporting period or explicitly reference the prior consumption year and precede audit fieldwork. Set your cancellation deadline first, then set your procurement deadline to allow enough time for registry processing – particularly for multi-entity or cross-border cancellations, which can take longer than single-registry transactions.

5.2 Choose Your Procurement Route

With your specification defined, the next decision is how to buy. There are three primary procurement routes available to European corporate buyers: spot or forward GO procurement, a corporate Power Purchase Agreement (PPA) and a utility green tariff. They are not mutually exclusive and most organisations use a combination. However, each suits a different buyer profile, and choosing the wrong route for your volume, geography, and quality requirements creates either operational complexity you cannot manage or credibility gaps you cannot close. The table below gives a quick orientation before each route is covered in full.

| Route | Best fit | Key trade-off |

|---|---|---|

| Spot / forward GOs | Most buyers; flexible volume and geography | Price uncertainty (spot) or commitment before consumption confirmed (forward) |

| Corporate PPA | Large, predictable baseload; additionality objective | Long-term commitment; credit and volume requirements |

| Green tariff | Distributed, smaller-scale, multi-country consumption | Credibility depends entirely on how the tariff is structured |

Spot and forward GO procurement

For most European corporate buyers, spot or forward GO procurement is the default route. It is operationally flexible, works across any volume, and can be executed across multiple national registries without a long-term contractual commitment.

The choice between spot and forward depends on volume, risk tolerance, and quality specifications:

- Forward purchasing works best for large buyers with predictable consumption and defined quality requirements. It provides price certainty and supply assurance before demand concentrates but requires committing before consumption data is fully confirmed.

- Spot purchasing offers flexibility for smaller buyers or those with variable consumption. The trade-off is price uncertainty and availability risk as the deadline approaches.

Timing matters regardless of which route you take. AIB data shows that peak cross-border transfer activity occurs between December and March, driven by annual disclosure deadlines. Buyers who delay procurement to that window face compressed availability and erratic pricing. A standardised forward market for GOs has existed since September 2024, giving buyers a hedging mechanism that was not previously available.

Corporate Power Purchase Agreements (PPAs)

A corporate PPA is a long-term contract between a renewable energy generator and a corporate buyer for the purchase of electricity output, typically with the associated GOs bundled in.

When a PPA fits and does not fit

→ PPAs are most appropriate for buyers with large, predictable electricity loads (broadly, baseload consumption above 50 GWh per year in a single geography), sufficient balance-sheet strength to absorb developer credit requirements, and a strategic objective to contract directly with a specific generating asset. A PPA with a new-build project gives the buyer a direct, documented link between their procurement and the construction of new renewable capacity, which carries weight under RE100 and SBTi frameworks and in voluntary disclosures.

→ For buyers with smaller volumes, geographically distributed consumption across multiple countries, or limited long-term visibility on energy needs, a PPA introduces complexity and risk that outweighs the benefits. Spot or forward GO procurement and potentially combined with green tariffs for operational simplicity, is the more practical solution for this profile.

GO transfer in PPA contracts

Most PPAs include the associated GOs as a bundled component, but this cannot be assumed. A PPA that does not explicitly transfer GO ownership to the corporate buyer may leave the buyer without the cancellation evidence required under ESRS E1-5. Any PPA negotiation should address GO transfer, the issuing registry, and who is named on the cancellation statement explicitly in the contract.

The ISDA EU Guarantee of Origin Annex, published in late 2025, provides a standardised framework for GO transactions within financial PPAs, integrating price hedging with certificate delivery20. This is expected to improve the bankability and tradability of PPA-linked GOs for buyers who want to separate the financial and physical components of their procurement.

Green Tariffs and Utility Products

A green tariff is a supply arrangement through which a utility or retailer provides electricity certified as renewable, backed by GOs procured on the buyer’s behalf. For companies with distributed, smaller-scale consumption across multiple countries, they offer a consolidated procurement route – but convenience and credibility are not the same thing.

The case for green tariffs

Green tariffs remove operational complexity. The supplier manages GO procurement, cancellation and registry documentation, and typically provides a certificate of supply for CSRD reporting. For companies with many smaller sites across multiple countries, a single green tariff arrangement consolidates what would otherwise require separate procurement across multiple national registries.

The credibility risk

The credibility of a green tariff depends entirely on how it is structured. A tariff backed by a specific generator or a defined pool of recently commissioned assets is meaningfully different from one backed by whatever is cheapest in the spot market at the time of procurement. ESRS E1-5 requires that the contractual arrangement clearly identifies the origin of the electricity. A tariff backed by an unspecified pool of legacy hydro GOs satisfies the legal standard but may not satisfy RE100, SBTi, or investor expectations. This distinction matters for audit readiness.

Before treating a green tariff as audit-ready evidence for CSRD reporting, request the following from your supplier. If the supplier cannot provide this information, the tariff should not be assumed to meet voluntary framework criteria or withstand scrutiny in an assurance review.

- The technology type and vintage of the underlying GOs

- The countries of generation

- Confirmation that the cancellation statement will name your legal entity as the beneficiary

Most buyers do not use one route alone. A common and practical approach is to cover large, predictable consumption through a PPA or forward GO contracts where quality supply is available, use green tariffs for distributed smaller sites where operational simplicity outweighs bespoke procurement, and fill residual volume with spot GOs close to the cancellation deadline. What matters is that every route in your mix produces cancellation documentation that names your legal entity, meets your quality specification, and arrives before your audit deadline.

5.3 Execute and Document

Choosing the right procurement route gets you to the right certificates. Executing correctly gets them into an audit-ready evidence package.

There is no single optimal sourcing pathway. The right route depends on the buyer’s procurement objective, governance needs and the type of supply being sought.

Exchanges and trading platforms give buyers access to listed supply at transparent, observable prices, typically through standardised contracts and centralised market infrastructure. This pathway is well suited to buyers that have already defined their procurement criteria and want to transact efficiently without running a full tender process.

Request for Proposals (RFPs) are structured competitive processes in which a buyer defines its requirements and invites suppliers to respond. This pathway is useful for larger or multi-year programmes where governance, documentation, and comparability matter as much as price. RFPs also create a documented rationale for supplier selection, which carries growing weight as climate claims face greater scrutiny.

OTC or bilateral deals are direct negotiations between buyers and sellers, offering maximum flexibility for bespoke terms and non-standard projects. This route can be useful where supply is highly customised, but it requires greater due diligence because price transparency is lower and counterparty reliance is higher than in standardised platform-based transactions.

Execute and settle

Buyers also need to determine how the trade will be processed, how settlement will occur, and where holdings will sit once the transaction is complete.

For buyers transacting on-platform, execution is typically more integrated, combining price discovery, trade submission, settlement tracking and holdings management within a single destination. This can shorten timelines, reduce manual handoffs, and make it easier to maintain a clear audit trail from trade agreement through to final use.

For buyers sourcing through RFPs or bilateral OTC transactions, execution may begin offline through structured tenders or direct negotiation. In those cases, post-trade support becomes just as important as the commercial negotiation itself. Settlement, delivery, and holdings management still need to be handled in a way that reduces operational friction and preserves a clean record of the transaction. A purchase negotiated offline may still be settled, held, or prepared for retirement through a third-party market infrastructure or service provider.

Well-designed execution processes shorten timelines, reduce manual handoffs, and make it easier to maintain a clear audit trail from trade agreement through to final use.

CIX Exchange

Experience a smarter, more flexible transaction platform, built to meet your evolving needs.

CIX offers end-to-end transaction support for EACs. Speak to us and design your best path forward with one of our experts.

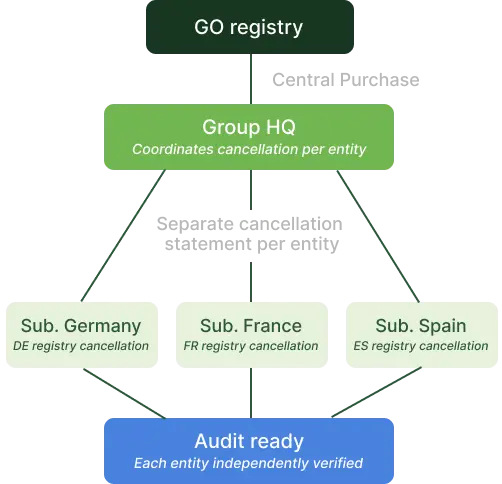

Multi-entity cancellation

For companies with multiple legal entities within their CSRD reporting boundary such as subsidiaries, joint ventures or branch offices across different countries, central GO procurement creates a documentation problem that surfaces at audit.

As established in Section 3.3, each legal entity in the reporting boundary requires its own cancellation documentation. A group treasury or procurement function that purchases GOs centrally and allocates them to subsidiaries in internal accounting creates a gap: the cancellation statement names the central entity, not the subsidiaries, and the auditor cannot verify renewable claims at the entity level where consumption occurred.

The solution is not to fragment procurement. Central purchasing still offers economies of scale and operational efficiency. The requirement is that cancellations are structured to name the correct beneficiary entity at the point of cancellation, not at the point of internal reallocation. In practice, this means working with the registry to process a separate cancellation statement for each legal entity in scope.

For companies operating across multiple countries, this adds a further layer: the entity consuming in Germany requires a cancellation through a German-domiciled or AIB-member registry, while the entity consuming in Spain requires a separate Spanish cancellation. For entities outside Europe, the same principle applies using the relevant local instrument with cancellation documentation naming the correct local entity. Registry processes for multi-entity, multi-country cancellations are not always straightforward, and buyers should factor this into their procurement arrangements well before their audit deadline.