Written by Julien Hall, Head of Intelligence, Climate Impact X

There is a distinct buzz in a growing corner of the carbon market – that of credits eligible under the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA).

For many voluntary carbon market developers and suppliers, it is refreshing to sell in a market where demand is driven by compliance, rather than a discretionary choice. Over the past 6-12 months, it has been fascinating to watch early trading dynamics evolve as CORSIA moved from theory to reality. A few observations are worth capturing.

Forwards dominate

Until November 2025, supply of CORSIA Phase 1 Eligible Emission Units (EEUs) was extremely constrained. Only one project had met the International Civil Aviation Organisation’s (ICAO) eligibility requirements: ART TREES 102, a jurisdictional HFLD (High Forest Low Deforestation) programme in Guyana. These credits traded on the spot market at a relatively steady $22-23/mt, but liquidity was thin and transactions sporadic.

With limited qualifying supply, most transactional activity last year took place through forward agreements, where developers pre-sold credits pending CORSIA eligibility for future delivery. These were typically priced at $14-19/mt, depending on whether a substitution guarantee was offered by the seller in the event eligibility was not secured.

The period also saw the emergence of index-linked pricing, with some transactions priced on a “floating” basis, usually either against the CIX CORSIA X benchmark or ICE December settlement values. This is a meaningful step toward the risk-management conventions of more mature commodity markets. I wrote in more detail about indexation in carbon markets in this piece.

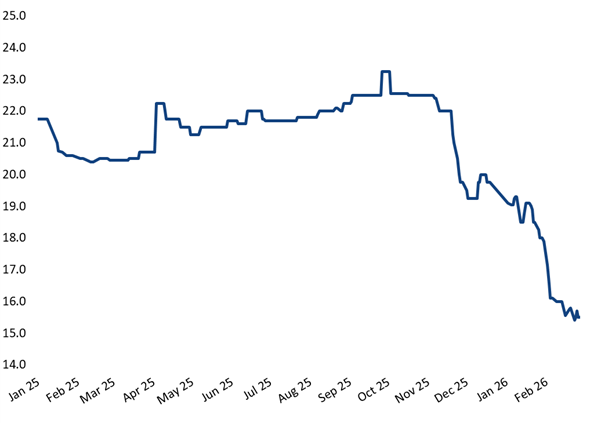

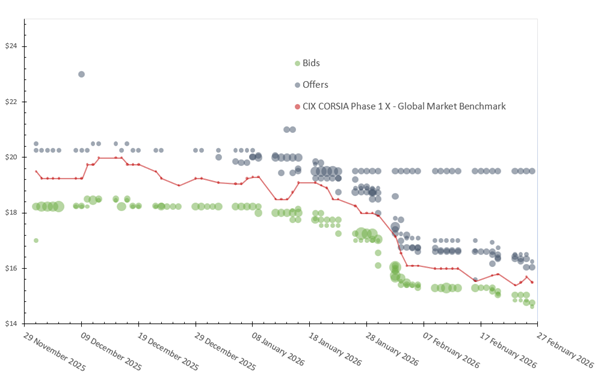

CIX CORSIA X price benchmark ($ per ton)

Birth of a spot market

The spot market came to life in November 2025 when additional projects qualified for CORSIA, including cookstoves projects developed by Hestian and Burn. Spot prices, previously anchored to ART 102, adjusted quickly as lower-priced supply entered. Credits from Del Agua – the first to be tagged by Verra – added significant liquidity on 30 January and triggered another dip.

Shortly after the Hestian and Burn labels were applied, CIX launched a daily screen-based spot contract (CIX CP1X-GM) on 1 December. The contract features firm, pre-funded bids and offers, helping enhance market transparency with a tighter bid-offer spread. Participation in the contract has steadily increased, though large-volume transactions still mainly occur off-screen.

While liquidity is still developing, screen-traded contracts are enabling airlines, traders and developers to transact in the spot market more efficiently and participate in open price discovery. Crucially, they generate high-quality datapoints needed to power robust benchmarks, materially improving overall price visibility (compared to the mainly forwards-based trading of 2025).

CIX CORSIA X benchmark alongside bids and offers on CIX spot contract ($ per ton)

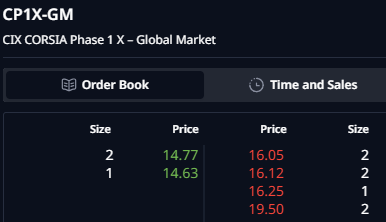

CIX CP1X-GM live order book on 27 February 2026 ($ per ton; size is in ,000 tons)

Project-level premiums

Even as trading venues improve transparency for generic, project-agnostic EEUs, specific projects have consistently been offered at 5-20% above the generic “benchmark” base price. The true clearing level of these premiums is unclear, but these project-level differentials have been a persistent feature since the second project became eligible.

Some of this may be a deliberate marketing strategy, some may reflect real demand factors. In commodity markets, primary producers often command a premium to secondary spot prices due to additional quality assurance and after-sales services. In the context of carbon, buyers may value direct capital flow to developers, regular project updates or marketing materials. Project types, methodologies and third-party project ratings may also influence perception of value.

From a pure compliance standpoint, any EEU satisfies CORSIA requirements. Many airlines are therefore project-agnostic. Others, however, apply additional filters to mitigate perceived regulatory or reputational risk. These risks may relate to uncertainty around EU’s ongoing review (concluding mid-2026), or sensitivity to media and stakeholder scrutiny. In practice, that can translate into preferences for credits from non-sanctioned jurisdictions, from countries where the airline operates, or from project types that align well with broader sustainability narratives.

In any event, it will be interesting to see the extent to which project-specific premiums persist as market liquidity deepens. Perhaps a key determinant will be what share of buyers end up being project-agnostic.

Price direction

Few market participants anticipated how quickly prices would fall once more supply came online. In 2025, the dominant narrative was scarcity, but the conversation has since shifted. While airline RFP activity has gradually picked up, actual procurement has remained generally subdued, likely contributing to weaker secondary spot market activity.

Market observers attribute this to continued uncertainty around CORSIA enforcement. Only a few countries have put in place penalties for non-compliance; the EU is still reviewing CORSIA and may opt to fold international flights into the ETS; while the US position remains ambiguous. Under the scheme, airlines will need to purchase between 146-236 million EEUs in the next 24 months according to IATA’s forecasts, pointing to some volatility ahead.

Meanwhile on the sell-side, also contributing to the initial price downtrend, some offtakers and investors holding early EEUs have been taking profit on their early positions, including presumably positions purchased in lower-priced forwards in 2025.

On paper though, supply remains tight with less than 20% of total expected Phase 1 demand currently available for purchase and retirement. Developers caution that bringing additional supply to market is challenging, as governments are understandably hesitant to grant carbon export permits without clearer visibility into their present and future carbon budgets.

Barring political intervention, both supply and demand are likely to accelerate in the months to come. The key question is how these fluctuations will translate into price movements. For those tracking developments, the CIX CORSIA X price benchmark is published in our complimentary carbon pricing report, CIX Carbon Daily. You can subscribe here.

Let’s Connect

Ready to discover the right price of carbon credits? Let’s connect.

Market Intelligence

"*" indicates required fields